Super Micro Computer (SMCI) got off to an incredible start this year as shares more than quadrupled from January to mid-March. This surge made Super Micro eligible for S&P 500 inclusion, with the technology hardware stock (with links to AI) being added to the index on March 18, 2024. In hindsight, that would have been a great time to take profits or Short the stock, as shares are down by more than 50% since then.

One of the major developments has been the report by Hindenburg Research, which contained worrying allegations about the company’s financial reporting. In assessing those allegations along with Super Micro’s fundamentals I hold a neutral rating on the stock.

Hindenburg Casts Doubts About Super Micro

The Hindenburg report is actually the main reason I am neutral instead of bullish on SMCI stock, and I believe it has caused hesitancy among many AI stock analysts and investors.

The accusations are pretty straightforward. According to Hindenburg, Super Micro engaged in accounting manipulation which included “sibling self-dealing and evading sanctions”. Anyone who thinks this sounds far fetched may wish to remember that the SEC charged Super Micro with widespread accounting violations in August 2020. Hindenburg’s report also argued that most of the people involved with that accounting malpractice are back on Super Micro’s team.

Hindenburg’s team interviewed several Super Micro salespeople and employees when compiling their report. It doesn’t help that Super Micro delayed its 10-K filing to assess internal controls shortly after Hindenburg went public with its concerns. While this might simply be a coincidence, the timing is worrisome. Looking back several years, Super Micro had failed to file financial statements in 2018 and was briefly delisted from the Nasdaq as a result.

Near the beginning of this month, Super Micro publicly issued a denial of the accusations, with CEO Charles Liang hitting back, stating that Hindenburg’s report contained, “misleading presentations of information”. Super Micro hasn’t provided any additional statements since then.

Artificial Intelligence Growth Is Undeniable

Super Micro’s status as part of the fast moving world of AI is one of the few reasons that I am neutral instead of bearish SMCI stock. The exciting prospects for the company’s business and the serious nature of the Hindenburg allegations basically offset each other.

It’s hard to know what’s real and what’s false here, but most people concede that the AI industry as a whole offers compelling growth prospects. Nvidia (NVDA) has been posting triple-digit year-over-year revenue growth for several quarters. Other tech giants have incorporated artificial intelligence into their core businesses and delivered impressive results for their shareholders. For instance, Alphabet (GOOGL) saw its cloud revenue rise by 28.8% year-over-year as many businesses rushed to create their own AI tools.

The artificial intelligence industry is also projected to maintain a 19.3% compounded annual growth rate from now until 2034, according to Precedence Research. The AI industry should continue to grow, and that should lift Super Micro. The company should benefit from Nvidia’s growth, which is why the company posted exceptional revenue and net income growth during Nvidia’s ascent. That’s what we saw for several quarters. We just don’t know how accurate all the numbers were, if the allegations targeting the firm have merit.

Super Micro Has Strong Financials at Face Value

While it’s impossible to overlook Hindenburg’s allegations against Super Micro, it’s still worthwhile assessing the company’s previous quarterly results. Shares were dropping even before Hindenburg released its report. While in March 2024 I argued that SMCI stock faced risks, I felt that shares presented a tremendous buying opportunity in late-summer, until Hindenburg muddied that optimism.

For its last reported quarter, Super Micro posted net sales of $5.31 billion, representing a 143% year-over-year jump. Meanwhile, net income rose by 82% year-over-year, reaching $353 million. At the time of the release, my primary concern was Super Micro’s declining net profit margin. Super Micro currently trades at a 20x trailing P/E ratio, seemingly enough to compensate for any further erosion in profit margins. SMCI stock has a ridiculously low 13.6x forward P/E ratio, but with the recent speedbumps (the Hindenburg report and DOJ investigation) investors seems reluctant to bid the valuation multiple any higher right now.

We don’t yet have tangible proof that Super Micro has engaged in any wrongdoing, as alleged by Hindenburg. Their report, however, has certainly cast a black eye on the stock. I expect that Super Micro would have significantly outperformed its fiscal 2023 results even excluding any misdealings.

The Department of Justice Is Probing Super Micro Computer

The Super Micro controversy added a new chapter on September 26, as news crossed the wires that the U.S. Department of Justice is now probing the company. SMCI stock tumbled an additional 12% on this news, and shares were recently trading at less than one-third of their all time high in March. There’s a high risk/reward on the shares at this point, but the elevated risks have relegated me to the sidelines with a neutral rating.

Super Micro shares bounced back by more than 4% on Friday, September 27, suggesting that many investors believe that the long-term potential for the business is worth the heightened uncertainty.

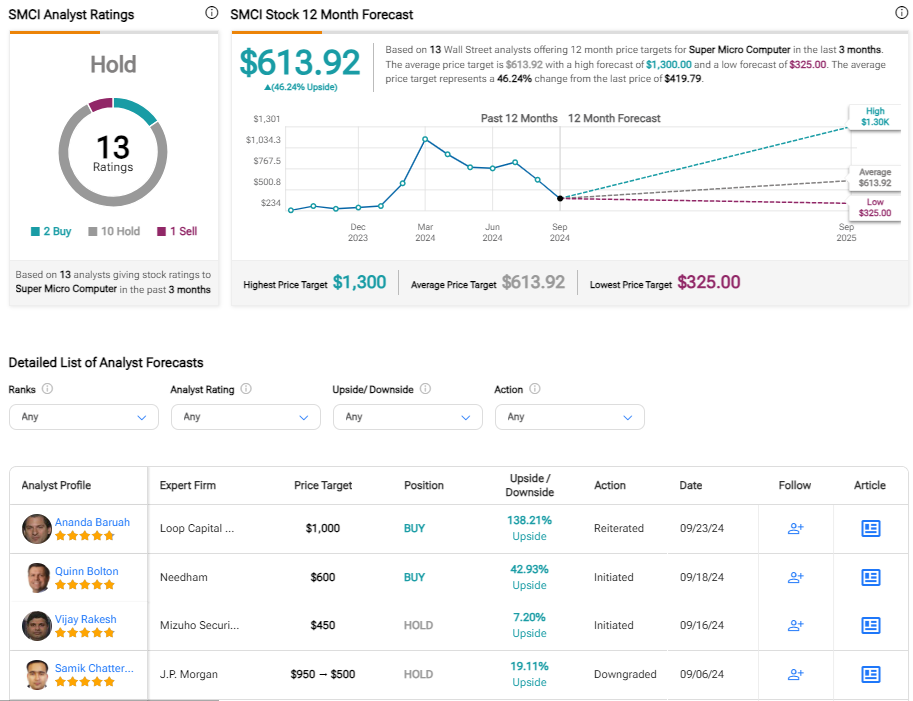

Is Super Micro Stock Rated a Buy?

Although the ratings for this stock could change quickly, Super Micro currently has 2 Buy ratings, 10 Hold ratings, and 1 Sell rating from the 13 analysts that cover the stock. The average price target for SMCI is $613.92, which implies potential upside of nearly 50%. Again though, it’s quite possible that several research brokerages have placed their SMCI ratings under review. SMCI stock does have a few low price targets including $454, $375 and $325 from CFRA, Wells Fargo (WFC), and Susquehanna respectively. All of these price targets were established before the DOJ probe was announced, so even they could drop lower.

The Bottom Line on SMCI Stock

There’s an old adage that suggests, “You either die a hero or live long enough to be the villain”. That quote seems apropos for this company. Super Micro earned many investors hefty profits during its rise above a stock price of $1,000 per share. Those who entered the story late, including after SMCI stock was added to the S&P 500, have not fared well. Many investors are sitting on significant losses right now. Depending on what those investors do, it’s hard to tell how much more downside Super Micro shares may have until more clarity on the ordeals is available.

If the company’s recent financials are accurate, SMCI shares look quite attractive here. Shares can surge quickly if the Hindenburg report loses relevance, although that outcome difficult to predict. I’m a big fan of Super Micro’s industry and business potential related to AI, which prevents me from being downright bearish. I have a neutral stance here. Meanwhile, I don’t expect shares of SMCI to rebound above $460 (the approximate price prior to news of the DOJ probe) without any resolution to the two main threats to shareholder value.